The Federal Reserve cut the Fed Funds rate by 0.25% this week, with more reductions likely ahead. As inflation cools and employment weakens, bond yields are already dropping. This is a problem for retirees: many bonds are callable, meaning issuers redeem them early and reissue at lower rates. Investors who held 5.5% and 5% bonds are seeing them called and replaced with yields closer to 4%.

For retirees relying on bond income—or taking RMDs—this environment means lower expected returns from balanced portfolios. And with U.S. stocks expensive and possibly due for a correction, conservative investors should not depend on equities for stable income.

Enter the MYGA

A MYGA (Multi-Year Guaranteed Annuity) is a fixed-rate annuity that behaves like a CD but often pays more. MYGAs currently offer rates in the mid-5% range and unlike many bonds or CDs, they are non-callable. That means your rate is locked for the full term (3–10 years), even if market yields fall.

Benefits of MYGAs:

Guaranteed fixed rate of return, non-callable.

Principal protection—very safe.

Tax-deferred growth until withdrawal.

Option for tax-free rollover at maturity (1035 exchange).

Creditor protection in many states.

Nearly 2% higher than comparable 5-year Treasury (5.6% versus 3.7%).

The Fine Print:

Limited liquidity; surrender charges for early withdrawals.

Some MYGAs allow interest to be withdrawn, others none.

Withdrawals before age 59½ may face a 10% IRS penalty on earnings.

Best suited for investors with sufficient liquidity elsewhere.

Why MYGAs Belong in Portfolios Now

With rates expected to trend lower, locking in today’s 5%+ yields through a MYGA can secure income for years. A callable bond at 5.5% may vanish if rates fall, but a 5.5% MYGA will not. This makes MYGAs particularly attractive for retirees and conservative investors looking for income stability.

Strategies for Using MYGAs:

Fixed Income Replacement: Substitute part of your bond allocation with a MYGA to boost yield and avoid call risk.

Laddering: Buy multiple MYGAs with staggered maturities to improve liquidity and reinvestment flexibility.

RMD Support: Use MYGA interest or partial withdrawals to help cover RMDs without tapping into equities in down markets.

Is a MYGA Right for You?

If you’re over 59 1/2, have significant fixed-income holdings, and don’t need immediate access to these funds, a MYGA may be an excellent fit. For many retirees, locking in 5%+ guaranteed and tax-deferred is far more attractive than taking chances on callable bonds or expensive equities.

The US stock market entered “correction” territory this week, with a decline of 10% from the recent peak on February 19th. Investors are concerned about the impact this will have on their portfolios and retirement plans. In today’s newsletter, we are going to share some facts about market corrections and give three strategies we use to help investors handle the market correction of 2025.

10% drops are common in the stock market. Over the last 125 years, there have been 56 market corrections. Of those 56 corrections, 22 went on to become a “Bear Market”, a drop of 20% or more. On average, we have a market correction every two years and a bear market every five years. It is not unusual for a correction to reverse course fairly quickly. Since 1980, the stock market was higher 12-months after a correction 81% of the time. The average gain, 12-months post-correction, was 13.4%.

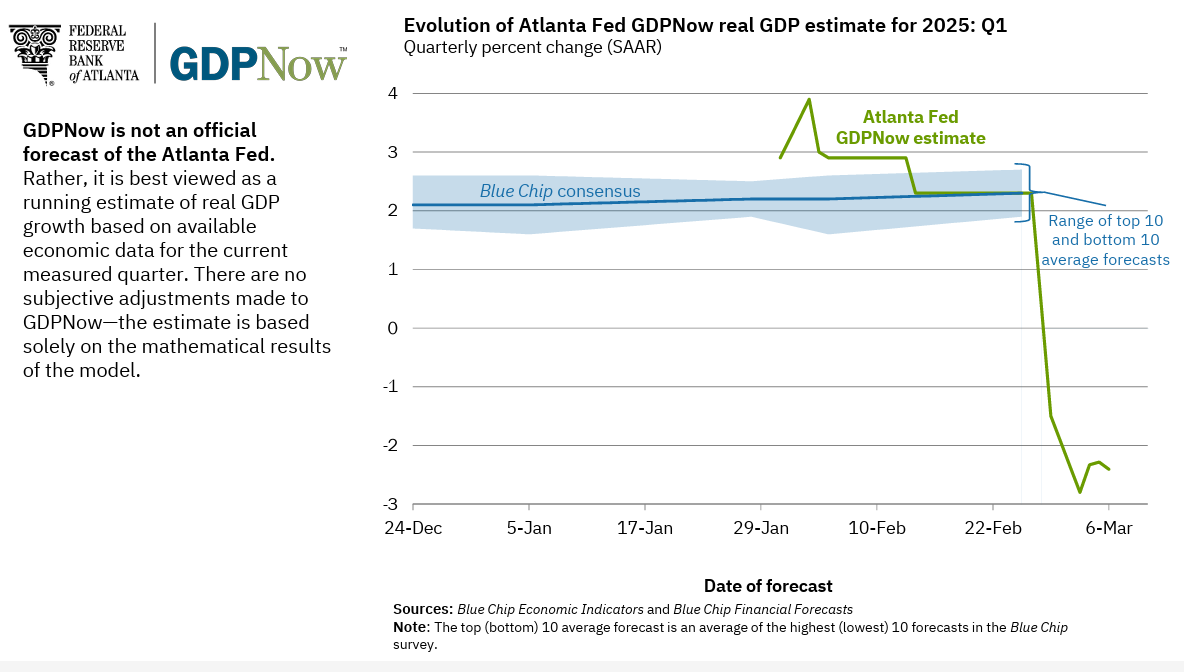

The outlook worsens somewhat if a recession occurs at the same time as a market correction. When this happens, the correction is often longer and more likely to develop into a bear market. The risk of recession has worsened over the past months. The Atlanta Federal Reserve has a statistical model to estimate GDP in real time, called GDPNow. At the end of January, they were projecting Q1 GDP would grow by nearly 3%. By March 6, this estimate has plummeted to -2.4%.

At this point, these are just projections. Still, investors’ appetite for risk decreases greatly when there is uncertainty. Today’s tariff plans, government cuts, and turmoil are certainly factors in the market correction of 2025. And frankly, US stocks had gotten very expensive and were ripe for a pull-back.

Strategies For Market Corrections

Where does this leave investors? Market corrections are a normal part of the investing cycle. Young and middle-aged Investors should do nothing. Don’t sell your funds, and whatever you do, don’t stop Dollar Cost Averaging in your 401(k) or IRA. There have been 21 market corrections since 1980. You should make no effort to “time” the market by trying to predict what you think will happen.

Market Corrections are often a great time to be adding to your diversified portfolio – in hindsight. At the present moment, fear is the more common thought than opportunity. But years from now, March of 2025 may look like an attractive time. (Five years ago, March of 2020 was horrifically painful at the time, but from today’s vantage, looks like an “obvious” opportunity.)

For Investors who are closer to retirement or in retirement, you have less ability to recover from a correction or a bear market. You may have income needs from your portfolio. This is why we advocate having a “Bond Bucket” consisting of individual bonds laddered from 1-5 years. This will provide all the income and withdrawals needed for the next five years, or longer. This allows us to leave our stocks alone during a market correction and not have to sell anything.

If the recent correction has you feeling you are too exposed to risk, what can you do? Here are three ideas:

A. Diversification

While the S&P 500 is down 4% year to date, International Stocks are up 9%. 5% of that 9% move is from the dollar falling against the Euro. While 2024 was all about US Tech stocks, performance has reversed in 2025. International is doing better than US. Value is now outperforming Growth. Equal Weight Indexes are doing better than Cap Weighted.

Here’s the thing about diversification: we don’t know when it is going to work. In years like 2024, performance is concentrated in a small number of stocks. Investors felt like diversification was hurting their performance, as International lagged US markets. However, these trends are eventually self-correcting. As one category becomes too expensive, another category becomes too cheap to ignore. Investors see International doing well, and sell their US funds and buy the International funds. This selling pressure depresses the US prices and increases the International prices. Remember, stock prices do not equal intrinsic value! Prices go up when there are more buyers than sellers. That’s it.

Our portfolios are highly diversified and the market correction of 2025 is showing why this is an important facet of portfolio construction. The temptation to chase performance often leads to worse results, and we prefer the patient, long-term approach of diversification.

B. Create Income

If you need retirement income from your portfolio, now or in the next couple of years, I suggest creating income from your portfolio. Stocks are highly volatile as we are seeing today. An aggressive portfolio of stocks carries a sequence of returns risk. That means that there is a higher chance of failure in retirement if there is a Bear Market at the beginning of your retirement. Stocks are great for long-term growth, but we don’t buy them for preservation and income.

In addition to the Bond Ladders mentioned above, another tool for retirement income is the Multi-Year Guaranteed Annuity, or MYGA. A MYGA is a fixed annuity, which guarantees you a rate of return for a set period. Today, we can purchase a 5-year MYGA at 5.60%. You can take out your interest monthly (great for retirees) or allow the MYGA to compound and walk away after five years. It’s tax deferred and there are no investment management fees. So, the 5.6% is your net return. MYGAs are non-callable, which is better than most bonds. (And according to several forecasts, 5.6% is higher than the expected return of US stocks for the next decade.)

We bought a lot of MYGAs in 2024 before the market correction of 2025. And I’m very glad we did. It’s not a magic bullet, but for those needing or wanting income, a MYGA is worth a closer look.

C. Index Funds

At every correction or downturn, Investors are tempted by the thought that an Active Fund could be more tactical or could profit from all the volatility in the stock market. It wouldn’t just sit there and do nothing. It could be defensive sometimes or more aggressive at others. It could avoid the loser stocks and stick with the winners.

Unfortunately, the data shows the opposite. Actively managed funds do worse than their benchmark. And the longer you invest the worse active funds do. The Standard and Poors Index Versus Active (SPIVA) report for 2024 was released this month. The study tracks all actively managed funds, including those which closed, for the past 20 years.

In 2024, 65% of Active US Large Cap stock funds did worse than the S&P 500. Over 10 years, that number increases to 84% and at 20 years, 92%. The lesson is clear: active managers do not add value. We are better off using low-cost index funds. If it was possible for mutual funds to time the market or only pick the good stocks, we’d see different results. It is less risky to stick with an Index Fund than to try to select an Active manager who you think will outperform.

Interesting Times

“May you live in interesting times” is a curse referring to times of turmoil and difficulty. Perhaps 2025 will qualify as interesting times. It feels like following the news could become a full-time job and that everything we are seeing is described as “unprecedented”. A lot of people feel overwhelmed and concerned.

Reacting to news, however, can be dangerous for your portfolio. We have a lot of history around market corrections to understand what is going on. They are a frequent, but temporary, interruption to the progress of global growth and productivity.

For investors who want to take additional steps to protect their portfolio, we have three recommendations. Diversify extensively, create income when income is needed, and stick with Index Funds. As unpleasant as market corrections are for investors, they are a natural part of the economic cycle. The key is having a good financial plan in place and then maintaining the resolve and patience to stick with the plan. All of this is very individual to your unique scenario, so please don’t hesitate to email me if you’d like to discuss things further.

How a fixed income annuity can provide guaranteed returns and predictable retirement income — especially for retirees in Texas, Arkansas, and nationwide.

A Multi-Year Guaranteed Annuity (MYGA) is a fixed-rate annuity that offers a guaranteed interest rate for a defined period — typically 1 to 10 years — making it a useful tool for retirees seeking predictable income or a safe place to grow cash. MYGAs are popular with conservative investors because they provide certainty in an uncertain market and can complement traditional retirement income sources.

How MYGAs Work (Straightforward Explanation)

A MYGA is an insurance contract in which you pay a lump sum upfront and the insurance company credits a fixed interest rate for a set term. Unlike market-linked investments, a MYGA offers stability — you know the rate and return ahead of time.

Here’s what this means:

You deposit a lump sum (often $5,000+; many competitive products start closer to $20,000+).

The annuity earns a guaranteed fixed rate for the term you choose (e.g., 3, 5, or 7 years).

Earnings grow tax-deferred until you withdraw them.

Upon maturity, you can take the money, renew into a new contract, or elect income payout options.

This makes MYGAs similar to CDs in principle — but with tax deferral and often higher rates.

Why Retirees Like MYGAs (Guaranteed Return and Safety)

MYGAs are especially appealing if you want:

Predictable, guaranteed interest income

Tax-deferred growth

A conservative portion of your retirement portfolio

Stability in a low-volatility product

Competitive Interest Rates: currently we offer a 5-year MYGA at 5.75%, a full 2% more than a 5-year Treasury Bond

Because returns are fixed, you don’t have to worry about market ups and downs affecting your principal during the contract term. For some retirees, guaranteed income products like MYGAs can complement laddered bonds and cash reserves within a well-structured retirement income planning strategy.

MYGA vs. CDs and Traditional Fixed Accounts

MYGAs are often compared to bank CDs, but there are important differences:

Feature

MYGA

Bank CD

Rate Guarantee

Guaranteed by insurer

FDIC/NCUA insured

Tax Treatment

Tax-deferred earnings

Interest taxed yearly

Income Options

Can convert to income

No lifetime income option

Liquidity

Limited, may have surrender charges

Early withdrawal penalty

Flexibility

Options at maturity

Less flexible

Based on typical product characteristics

MYGAs are backed by insurance companies and state guaranty associations — not FDIC insurance — so the financial strength of the issuer matters.

How MYGAs Can Fit Into Retirement

MYGAs can provide predictable income or serve as a safe allocation within a broader retirement income plan. This can include:

🔹 Income Planning

If you want a fixed stream of interest income during early or established retirement, a MYGA can fill the gap between Social Security, pensions, or RMDs.

🔹 Laddering for Predictable Cash Flow

Buying MYGAs with staggered maturities ensures you can take money or reinvest at regular intervals — similar to a bond ladder.

🔹 Risk Reduction

Because returns are fixed, they provide stability in an otherwise volatile market.

MYGAs aren’t right for everyone. Key considerations include:

🔸 Liquidity and Surrender Charges

MYGAs typically have surrender periods during which withdrawals beyond a penalty-free amount may incur charges. Read the contract carefully.

🔸 Tax Considerations

Growth is tax deferred, but withdrawals are taxed as ordinary income. If you withdraw before age 59½, you may face a 10% IRS penalty on earnings.

🔸 Insurer Strength

Check the insurer’s ratings and the state guaranty association coverage limits.

These features underscore why it’s smart to work with a fiduciary who can match product features to your personal situation.

Why Consider a MYGA With Us (Texas, Arkansas & Nationwide)

If you’re a retiree seeking income — even if you’re not looking for full wealth management — MYGAs can provide competitive fixed income options with market-leading interest rates. Our access to top annuity carriers means clients in Texas, Arkansas, and across the U.S. can secure highly competitive rates and terms that align with their income goals.

We help you:

Evaluate options across multiple products and terms

Compare surrender periods, riders, and features

Make decisions aligned with your risk tolerance and income timeline

MYGAs can be a standalone retirement income solution or a component of a broader plan. Whether you want a safe place for excess cash or a predictable income stream, we can help you explore whether a MYGA fits your needs.

For broader retirement planning that addresses sequence of withdrawals, taxes, and longevity risk, check out our Retirement Income Strategy and our Who We Help pages.

Frequently Asked Questions

What rate can I expect on a MYGA in 2026?

Current competitive MYGA rates are about 5.75% for a 5-year and depend on term and issuer. These rates can be materially higher than traditional CDs or short-term bonds. They also vary quite a bit from insurer to insurer, so it can pay to have an independent agent who can shop around for the best rates and features.

Are MYGAs safe?

MYGAs are backed by insurance companies and state guaranty associations, not the FDIC. It’s important to review the issuer’s rating and the contract terms.

Can I use a MYGA for retirement income?

Yes. MYGAs can provide predictable income or supplement your other retirement income sources when structured appropriately.

How do you begin to think about safe investing during deflation? Last week, the US Bureau of Labor Statistics reported that the CPI-U fell 0.8% in April. The Consumer Price Index is a basic measure of inflation and has almost always been positive throughout US History. Deflation is not a good environment for building wealth.

While this could be a temporary blip due to falling energy prices in April, we certainly are not out of the woods from the economic damage of the Coronavirus. With 20.5 million people filing for Unemployment in the last two months, there could be an extended reduction in consumer demand. And we know from Econ 101 that when demand shifts down, there becomes an oversupply of goods, and prices fall. That’s deflation.

I think that any deflation will be temporary and that the global economy will recover. But the amount of time this takes could be anywhere from months to years. And while I am studying projections of the depth and duration of this likely recession, my readers know what I think about expert predictions. They are wildly inaccurate. Trying to time the market based on economic predictions is likely to do worse than staying the course.

Deflation Is Anti-Growth

What might deflation mean for investors? Historically, stocks do poorly during deflationary periods. Commodities and Real Assets also can lose value. If millions of people lose their jobs and income, how are they going to afford a mortgage and buy a house? We know from 2008 that house prices can go down when people cannot buy houses.

No one has a crystal ball to know what will happen next. But, I think investors can and will want to make small adjustments to their investment portfolios because of the possibility of deflation. With the market rebounding incredibly well from the March lows, the upside versus downside potential in the near term has worsened.

It is okay to want to have some of your investments in a safe asset. The challenge that we discussed in the previous blog is that we are near zero percent interest rates today on cash, CDs, and Treasury Bills. While this would technically preserve purchasing power in a deflationary environment, we can do better and should be looking to grow.

Fixed Annuities For Capital Preservation

My suggestion for a safe yield today: fixed annuities. This week, I had a client purchase a 5-year annuity at 2.9%. That is 2.6% higher than a 5-year Treasury bond today (0.307%). Both are guaranteed, yet the annuity gets a bad rap. Sometimes, an annuity is the right tool for the job. Sometimes, it is not. Unfortunately, because some unscrupulous salespeople sold annuities which were unsuitable for the buyers, investors have negative perceptions.

I keep bringing them up because they are an objectively effective fixed income solution that many savers would appreciate. Because I want every investor to make informed decisions, here is what you need to know about Fixed Annuities.

Annuity Basics

An annuity is issued by an insurance company and is a contract between the company and you. There are many flavors of annuities, but the kind I am discussing today are Fixed Annuities, specifically Multi-Year Guaranteed Annuities (MYGAs).

A MYGA has a set term (3, 5, 7, or 10 years commonly) and a fixed rate of return. In this aspect, it behaves similarly to a CD.

An Annuity is a tax-deferred retirement vehicle. You will not pay any taxes on the gains from the annuity, until you withdraw the money. At the end of the term, you can roll into a new annuity and continue to defer the gains. This is called a 1035 Exchange. There are no income restrictions or contribution limits to annuities.

If you withdraw from an Annuity before age 59 1/2, there is a 10% penalty on the gains. Annuities are most popular with investors over 55, but younger people who know they are not going to need the money until retirement can also use a MYGA towards retirement saving. You can invest IRA money (Traditional, Roth, etc.) into an Annuity, too.

There are often large penalties if you withdraw money from an annuity before its term is complete. For this reason, it is very important to have other sources of liquid assets. That way you can remain in the annuity for the full term.

What happens if an Insurance Company fails? Annuities are insured at the State level by a mandatory Guaranty Association. In Texas, all insurers pay premiums to the Texas Guaranty Association, which protects annuity holders up to $250,000. This information is for educational purposes only and is not an inducement to buy insurance. If you have more than $250,000 to invest, spread your money over several insurance companies to stay under the covered limit.

How to Use MYGAs

A MYGA is a good substitute for a bond or bond fund. They offer safety and capital preservation, but with a higher rate of return than cash, CDs, or T-Bills available today. While there are some corporate and municipal bonds with higher yields, they are generally not guaranteed and carry risk that the issuer could default and be unable to pay. That’s especially a problem during deflation, as bankruptcies could increase significantly, causing losses to bondholders.

The main trade-off with MYGAs is the lack of liquidity. We want to keep annuity purchases to a reasonable size. I also recommend creating a 5-year ladder, where you divide your total investment into 5 pieces which will mature in 1,2,3,4, and 5 years. Then in each subsequent year, you will have access to 20% of your investment, should you need it. And what you don’t need, you can reinvest into a new 5-year annuity at the top of the ladder.

Lastly, for transparency, Annuities pay a commission. If someone purchases a MYGA from me, the insurance company will pay me a commission on the sale. I generally view commissions as a conflict of interests. However, I’d point out that a 2.9% yield on a MYGA is the net return to the investor.

There are no investment advisory fees for Annuities. For some reason, I don’t hear very many Investment Advisors mentioning that to their clients when they bash Annuities! I want what is going to be best for you. If that’s an annuity, fine, and if not, that’s fine too. echo The minimum investment on most annuities is $10,000, but if you have a smaller amount, let me know.

Stay Diversified, Increase Safer Positions

Safe investing during deflation can be a challenge. Low interest rates aren’t helping investors. I will continue to recommend diversified portfolios which may have 50% or more in stocks for long-term investors. Still, there is a role for safe investments for most portfolios, and many people may want to have more safe investments. They offer ballast against the risk of stocks and the diversification can give a smoother trajectory to your overall return.

Given the strong rebound we have had from the March 2020 crash, this may not be a bad time to reevaluate your risk profile. If that thought process has you wondering about safe investing during deflation, lets talk about MYGAs. I am an independent agent and can offer annuities from many different companies to find you the best features and rate for your needs.