If you have a significant estate and are thinking about how to give money to charity or individual beneficiaries, you might want to consider if it would be possible to make some of those gifts during your lifetime. Today, we are going to look at the tax benefits or implications of different large gift strategies.

A gift to charity from your estate will reduce your your taxable estate. However, with the estate tax threshold presently at $11.4 million per person, most people will never pay any estate taxes. This was not the case 15 years ago when the estate tax threshold was just $1.5 million. For married couples, the threshold is doubled to $22.8 million. So if your past estate plan was based on estate tax avoidance, it may be time to update your plans and revisit your charitable strategies.

Charitable donations remain eligible as an itemized deduction, although many tax payers will not have enough deductions to exceed the 2019 $12,200 standard deduction ($24,400 married). However, if you are contemplating a large charitable donation, you can deduct up to 60% of your Adjusted Gross Income (AGI) when making a cash donation to a public charity. (This was increased from 50% under the 2017 Tax Cuts and Jobs Act.) If making a donation of non-cash property, such as appreciated shares of stock, the limit is 30% of AGI. In both cases, you can carry forward any excess donation for five years.

Here are seven principles for giving to charities and to individuals, such as your children or grandchildren:

1. If you have stocks or funds with a large gain, you can give those shares to charity, get the full tax deduction and avoid capital gains tax. The charity will not pay any taxes on the shares they receive and sell.

2. If you leave an IRA to a charity, that is name a charity as a beneficiary of your IRA rather than a person, they will pay no tax on receiving your IRA.

3. For individual beneficiaries of your estate, they will have to pay income tax on inheriting your IRA. Presently, there is a Bill which has passed the House which will eliminate the Stretch IRA. However, beneficiaries will receive a step-up in cost basis on inherited taxable accounts. The most tax efficient split is to leave your Traditional IRA to charity and your taxable assets and Roth IRAs, to your heirs. Then neither will pay income taxes on the assets they receive.

Read More: 7 Strategies If the Stretch IRA is Eliminated

4. If you are over age 70 1/2, you can make up to $100,000 a year in gifts from your IRA as Qualified Charitable Distributions, which count towards your RMD. You do not have to itemize to use the QCD.

Read More: Qualified Charitable Distributions From Your IRA

5. You can give $15,000 a year to any individual; this is called the annual gift tax exclusion. A couple could give $30,000 to an individual. This includes your adult children. Additionally, you can directly pay medical or educational expenses for any individual without this limit.

Where many people are confused: exceeding the gift tax exclusion does not automatically require you to pay a gift tax. It simply requires filing a gift tax return, which will reduce your lifetime Gift/Estate tax limit, which again is $11.4 million per person (2019). For example, if you give someone $17,000 this year, the $2,000 over the $15,000 limit will be subtracted from your $11.4 million estate tax exemption when you die.

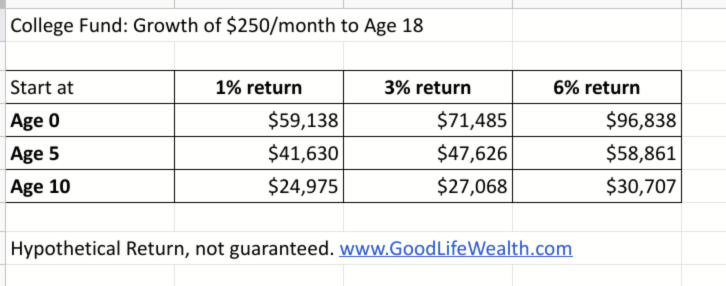

6. If you want to create college funds for your grandchildren or other relatives, you can fund up to five years upfront into a 529 Plan without exceeding the gift tax exemption. That is $75,000 per beneficiary, or up to $150,000 if coming from both Grandma and Grandpa. You can retain control of the funds, even change the beneficiary if desired, and the money grows tax-free for qualified higher education expenses.

Read More: 8 Questions Grandparents Ask About 529 Plans

7. You can make a large donation to a Donor Advised Fund to receive an upfront tax deduction and then make small donations in the years ahead. For example, it would be more tax efficient to make a $100,000 donation into a DAF and make $10,000 a year in charitable distributions for 10 years from the DAF, than to make regular $10,000 donations each year for 10 years.

Read More: Charitable Giving Under The New Tax Law

Even if you know all of this information, I think many potential donors are still looking for more flexibility in their giving plans. What if you need money later? How much should you keep for your own expenses and needs? Creating a comprehensive retirement analysis is an essential first step, and then we can help you consider other more advanced giving strategies.

There are many ways of structuring charitable trusts which can split assets and income between the creator of the trust, a charity, and/or beneficiaries. Generally, the donor is able to receive an upfront tax deduction for the present value of a gift, based on their expected lifetime or duration of the trust. The present value is calculated using your age and a specific discount rate, known as the Section 7520 rate, which is published monthly by the IRS. It is based on intermediate treasury bonds and is currently 2.2% for trusts created in September 2019. This rate is down from 3.4% from last August.

With a very low interest rate being used for the discount rate today, it is quite unappealing to establish a Charitable Remainder Trust (CRT). The low rate means that the tax deduction is very small compared to trusts that were established when the rate was higher. That’s unfortunate, because a CRT is an ideal structure: the creator receives income from the trust for life (or a set period of years) and then the remainder is donated to the charity when you pass away (or at the end of the term).

A more effective structure for a low interest rate environment is a Charitable Lead Trust (CLT). In this type of trust, a charity receives income for a period of years (say 10 years) and then any remaining principal is distributed to your beneficiaries, free from gift or estate taxes. This might hold some appeal for tax payers who would be subject to the estate tax and who do not need or want income from some portion of their assets. But it doesn’t offer much appeal to donors who want income or flexibility from their trusts.

If you are thinking about charitable giving or where your money might eventually go, let’s talk about which strategies might make the most sense for you.