Each year, we share our thoughts on the investment markets and where we see areas of opportunity for the year ahead. This letter is not intended as a short-term market forecast—no one knows what markets will do over the next few months. Instead, it outlines how we think about long-term expected returns and how that informs our portfolio positioning.

Our investment process is based on tactical asset allocation. We modestly overweight asset classes that appear to offer more attractive long-term expected returns and underweight those that appear more expensive and less attractive. Throughout this process, we remain fully invested in diversified, buy-and-hold portfolios. We do not try to time the market.

We continue to believe in the benefits of using low-cost, passive Exchange-Traded Funds (ETFs) and focusing on what we can control: saving consistently, keeping costs low, maintaining tax efficiency, and staying disciplined through market cycles.

(You can view last year’s investment themes here.)

Expected Returns for the Decade Ahead

We believe it is largely unproductive to try to predict where the stock market will be over the next 3–12 months. In the short run, markets move based on supply and demand—prices rise when there are more buyers than sellers and fall when the opposite occurs. Short-term price movements are often noisy and emotional, and prices do not always reflect underlying value.

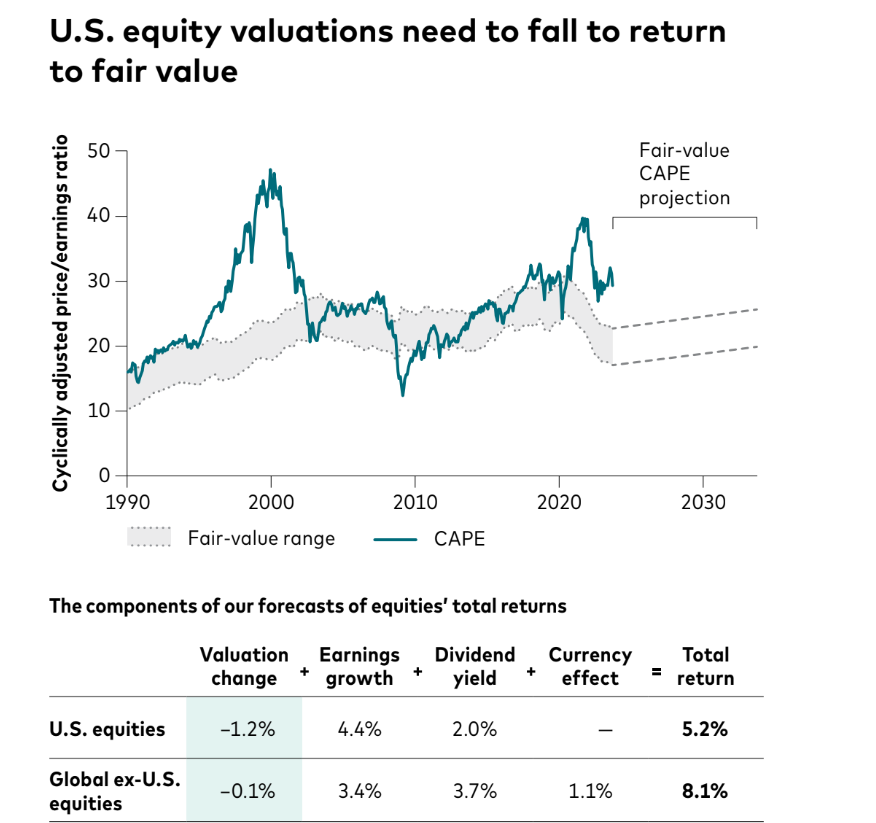

What does matter to us is the outlook for long-term expected returns over the next 5–10 years. This longer time horizon helps tune out daily headlines and instead focuses on valuation—whether today’s prices are high or low relative to future growth expectations.

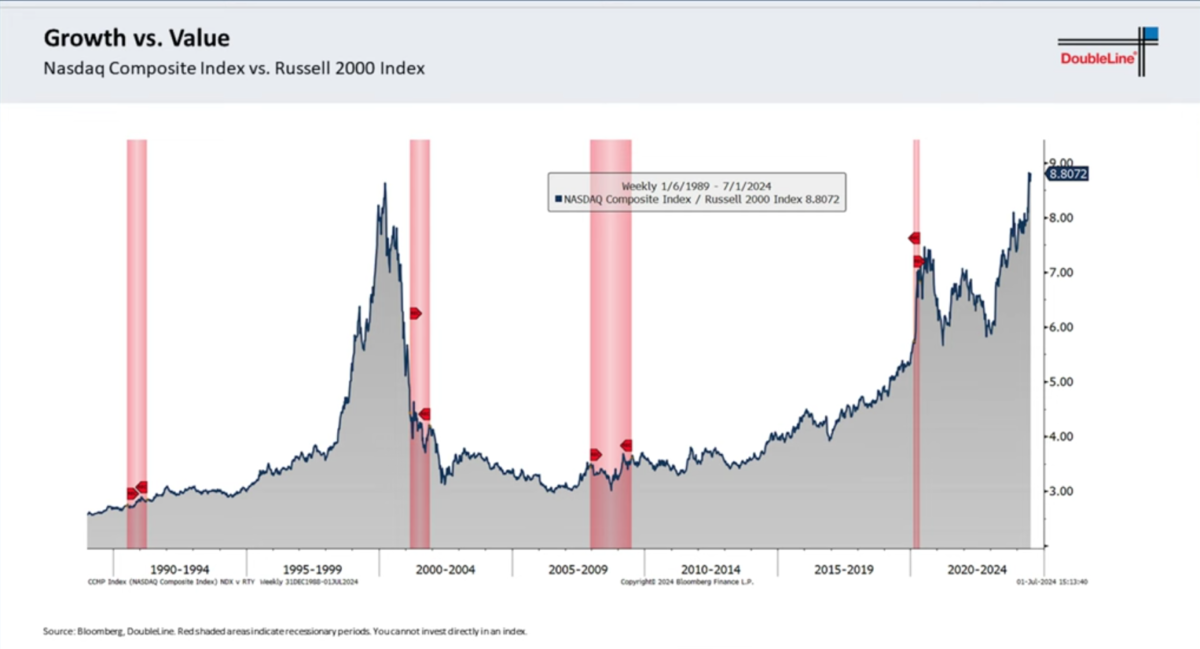

Today, U.S. growth stocks appear expensive by historical standards. The so-called “Magnificent 7” (Google, Amazon, Apple, Meta, Microsoft, Nvidia, and Tesla) have driven much of the U.S. market’s strong performance in 2024 and 2025. These companies now represent a very large share of the S&P 500, and their outsized gains have likely pulled forward many years of anticipated earnings growth.

We do not know whether this will result in a sharp correction or simply a period of more modest returns. What history consistently shows, however, is that high starting valuations tend to lead to below-average returns over the decade that follows.

Vanguard’s current estimates for annualized returns over the next decade are as follows:

- U.S. Growth Stocks: 1.3% – 3.3%

- U.S. Value Stocks: 5.3% – 7.3%

- U.S. Small Cap Stocks: 4.3% – 6.3%

- Developed Markets (ex-U.S.): 5.3% – 7.3%

- Emerging Markets: 3.2% – 5.2%

How We Are Positioned for 2026

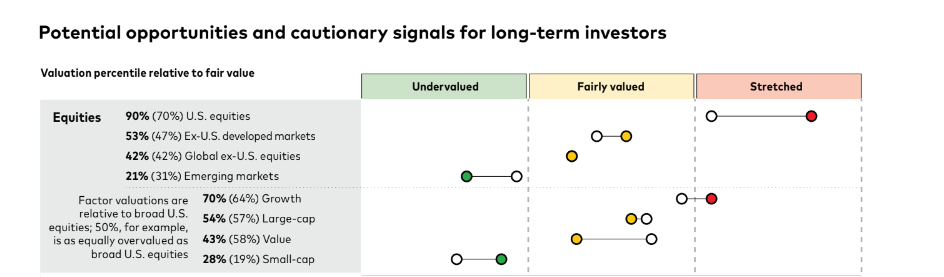

Our portfolios remain globally diversified, typically using approximately 10 ETFs. We have already been positioned toward areas of relative opportunity, so changes for 2026 are modest. Specifically, we are shifting a few percentage points from U.S. stocks toward international stocks.

We remain overweight U.S. value stocks and underweight U.S. growth stocks. Relative to global benchmarks, we are overweight international equities, including a meaningful allocation to emerging markets and a smaller allocation to international small-cap value stocks.

International stocks were our strongest performers in 2025, significantly outpacing U.S. stocks. We believe 2025 may have marked an important turning point after many years of U.S. outperformance relative to international markets.

On the fixed-income side, interest rates have declined at the short end of the yield curve as the Federal Reserve has begun cutting rates. With a new Fed Chair expected to be appointed this year, it appears likely that monetary policy may remain accommodative.

Credit spreads—the difference in yield between Treasury bonds and lower-quality corporate bonds—remain very tight. As a result, we see limited compensation today for taking additional credit risk in high-yield bonds.

Our bond portfolios are therefore unchanged for 2026. They consist primarily of a laddered portfolio of high-quality bonds with maturities ranging from one to five years, including Treasury, Agency, and A-rated corporate bonds. For investors seeking dependable income without liquidity needs, five-year fixed annuities continue to offer some of the most attractive “safe” yields available today.

Many portfolios also include smaller allocations to Treasury Inflation-Protected Securities (TIPS), emerging-market bonds, and preferred stocks. Overall, bonds continue to serve their intended purpose: providing stability and income, while equities remain the primary driver of long-term growth.

Lessons from 2025

The past year was not what most experts predicted, and it serves as an important reminder of what truly matters for investors: staying diversified, sticking to the plan, and avoiding emotional decisions.

While 2025 is ending as a very strong year—with double-digit returns in both U.S. and international stocks—it is easy to forget how challenging it felt at times. In April, markets were nearly 20% below their highs, and many economists were forecasting severe economic damage from new tariffs. Investors who panicked and sold during that period missed out on substantial subsequent gains.

The lesson is clear: long-term investors have historically been rewarded for discipline, not for reacting to short-term fears. (This applies to diversified portfolios like the ones we use; individual stocks, of course, can and do fail.)

2025 also marked a resurgence of diversification. While the S&P 500 is up roughly 19% year-to-date, international stocks (EAFE Index) are up approximately 32%. Investors who assumed 2025 would simply repeat 2024 missed out on these gains. Diversification remains one of the most reliable tools we have—because no one can consistently predict which asset class will lead in any given year.

Often, the hardest part of investing is having the patience to do nothing. In 2025, buy-and-hold investing worked exactly as intended, despite constant negative headlines. While we never ignore economic or political risks, we allow those concerns to be reflected in valuations and expected returns rather than reacting emotionally to every news cycle.

Looking Ahead

2025 was an outsized year, and it would be unrealistic to expect markets to deliver 20–30% returns every year. While we would welcome another strong year in 2026, it is more prudent to expect more modest returns and an eventual reversion toward long-term averages. Investors can still be very successful with steady, market-level returns over time—the key is remaining invested through both good years and difficult ones.

We are grateful for the trust you place in us to manage your investment portfolio. I follow the markets closely so you don’t have to, and I am always happy to discuss our investment philosophy, portfolio positioning, or any questions you may have.

We will continue to monitor portfolios carefully throughout 2026 and make adjustments as conditions warrant. Thank you for your continued confidence and partnership.

")