Do you have a college fund set up for your children or grandchildren? It is back to school time and that’s a little bit different this year. No one knows if the online classes will permanently change the process of education in the world. Still, I think there will be no substitute for the career benefits of having a degree in an in-demand field from a top notch school. Not everyone needs college, but overall, a higher education is strongly correlated to future earnings and career satisfaction.

The cost of a college education continue to climb. Student debt has become a crippling problem for many young adults I meet. They were told it would be worth it to get their degree, regardless the expense or their future earnings potential. Every parent wants the best for their kids, for them to have the opportunities we did not have. We want for them to be able to pursue their dreams and find their own unique greatness. Helping to pay for college goes a long way to setting up your kids to find their own Good Life.

Like most big financial goals, I think the best way to create a successful college fund is by making it automatic. Establish a 529 college savings account and make automatic contributions each month. If you can only start with $100 a month, great, just get started. Later, you can gradually bump that up to $200 or $300 a month or more.

How Much Should You Save?

A 529 plan will allow you to invest into a diversified allocation. The 529 Plan I use has Vanguard, iShares, and State Street index funds, just like I recommend in our Premiere Wealth Management portfolios. While no one knows future returns, let’s consider how your money might grow at 1%, 3%, or 6%. And then let’s also consider if you start at age zero, 5, and 10 for your kids. This would equate to 18, 13, and 8 years of growth to age 18 and the start of college.

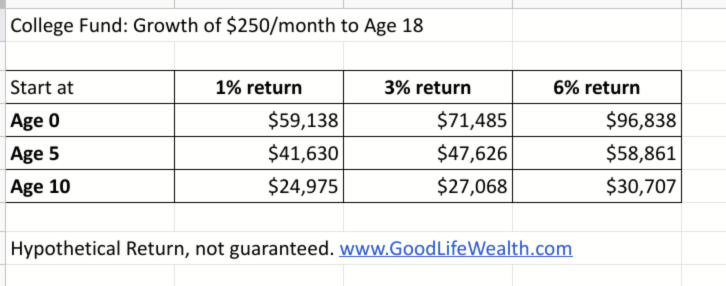

Here is how $250 a month would grow:

There are two main points I think this chart makes. First, it pays to start your college fund early for compound interest. If you wait until your kids are 10, you might have only one-third the amount saved, compared to starting at birth. Second, you aren’t going to grow much if your money is in a bank account earning one percent. (By the way, at $250 a month, or $3,000 a year, you would have contributed a cumulative $54,000 over 18 years, $39,000 over 13 years, or $24,000 over 8 years.)

How to Get Started

A 529 College Savings Plan is an efficient way to create a College Fund, as distributions for qualified education expenses are tax-free. You can even start a 529 for an unborn child and change it to their name once they are born. The important thing is to get started early. Each state sponsors their own 529 Plan. If your state has income taxes, there may be a benefit for using the In-State plan. For Texas, since we don’t have an income tax, there is no inducement to use the Texas plan versus one from any other state. You can use any plan at any college in the country.

While you could save in a regular account for college, there are valuable tax benefits in 529 Plans. Most investors prefer to have different buckets for different goals. This helps address savings goals. Even if your kids are 10 or older, it’s not too late to start your college fund. We are accepting new clients and want to help you get started.

If you’d like an estimate what it might cost to send your kid to a specific University, send me that information. I’m happy to prepare a report for you. We will estimate future costs and calculate a saving and investing plan. (Be prepared to be shocked if you plan to pay for 100% of four years at a private university.)

Learn More About 529s

Looking for details on how a 529 Plan works? Here’s what you need to know.

Want to compare different 529 Plans? Check out SavingForCollege.com

529 Plans are a way for Wealthy Families to create an inter-generational transfer of millions of dollars, potentially tax-free. This linked article calculates that parents who fund $1 million dollars into 529 Plans could be able to cover the college educations of four grandchildren, eight great-grandchildren, and 16 great-great-grandchildren. That’s because when you over-fund a 529 plan, you can always change the beneficiary to a younger generation later. The successor owners of your 529 Plans can keep the accounts open and change beneficiaries, even after you are gone.