Updated for 2026 — Planning-first language for retirees and pre-retirees

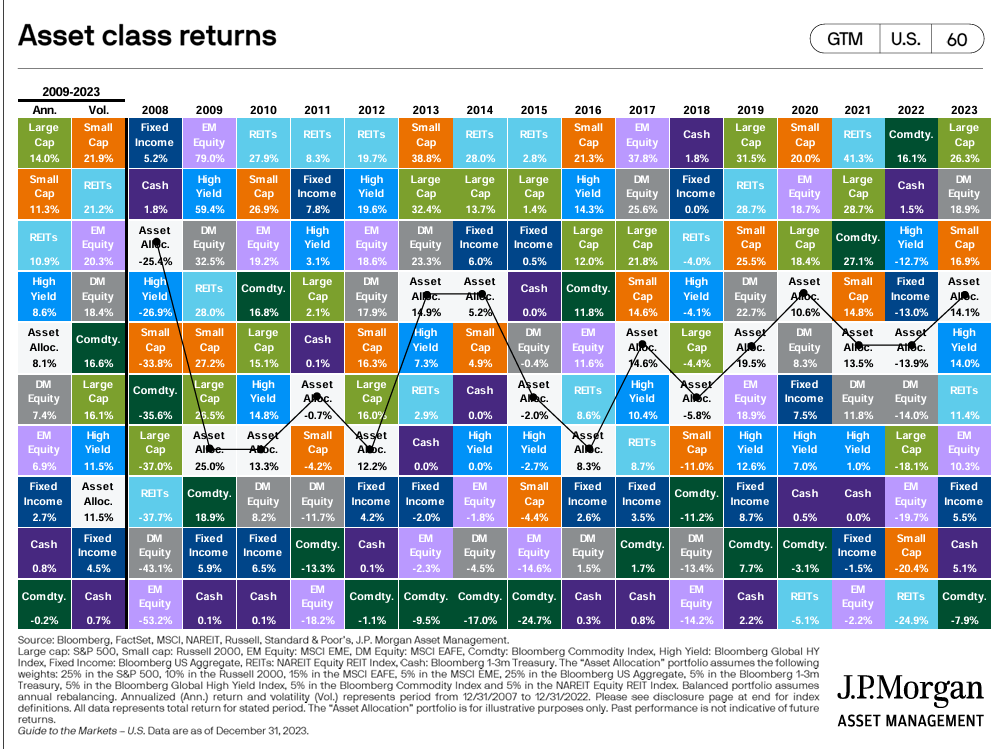

Many retirees and those approaching retirement find themselves checking account statements after a strong year in certain market segments — especially when one area (like large growth stocks) outperforms nearly everything else. The chart below, sourced from J.P. Morgan, vividly illustrates how the top-performing investment categories change from year to year (2008–2023), including U.S. stocks, developed and emerging markets, bonds, real estate, commodities, and cash.

Why Performance Chasing Is Especially Dangerous for Retirement Investors

When a particular category outperforms one year — and especially in hindsight when it “looks obvious” — it can be tempting to shift away from a broadly diversified portfolio into what just worked best. This behavior is known as performance chasing:

- It treats recent winners as future winners, even though history shows that last year’s top performer often underperforms in subsequent years.

- It increases the risk of selling diversified holdings after declines and buying into areas that have already risen substantially.

For retirees and pre-retirees, the stakes are higher than for many accumulators. Changing allocations based on recent performance can increase the risk of sequence-of-returns losses — when poor returns early in retirement can have an outsized impact on long-term spending sustainability.

Contrast this with diversification, where owning multiple asset categories — even ones that lag in the short term — tends to smooth returns and lower overall risk over the long run.

Past Performance Is Not Predictive — Especially Near Retirement

It’s common for investors to see a chart like the one above and think:

“I should sell my diversified portfolio and buy the top performer from last year.”

This is performance chasing — abandoning a long-term, diversified strategy because of recency bias. Over short spans, certain assets may shine, but over time, no single category consistently outperforms.

Diversified portfolios are structured so that gains in some areas weathers declines in others. While this means you won’t always be in the leading category each year, it also reduces the risk that you are overly concentrated in one bucket — particularly important when you are drawing down assets in retirement.

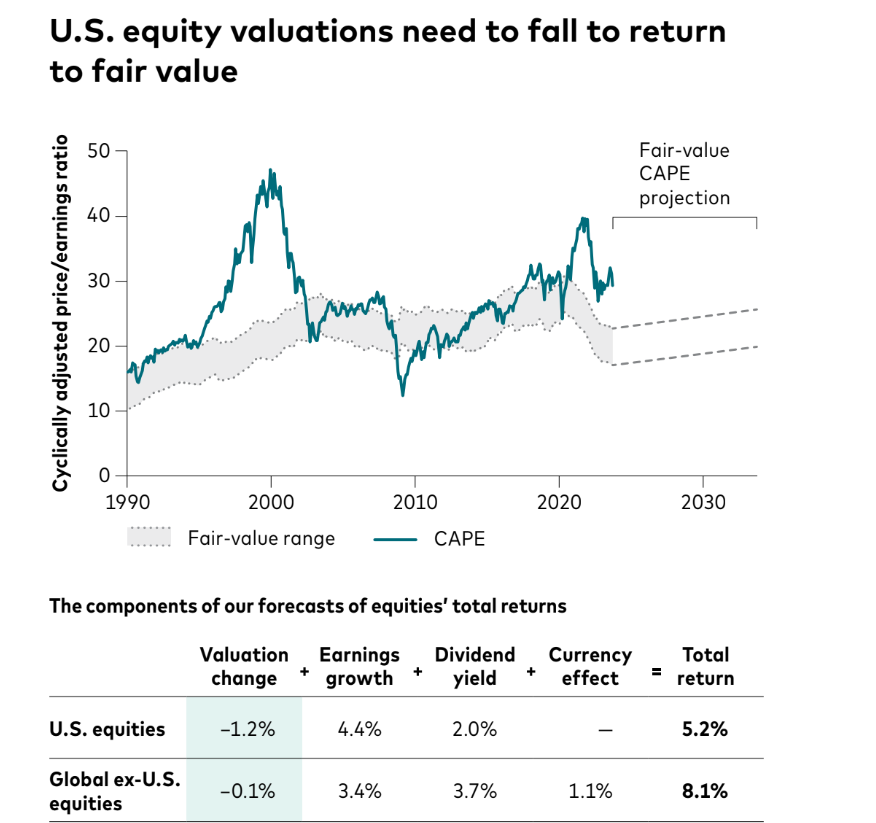

Valuations Matter — But Timing the Market Doesn’t Work

Behavioral biases often cause investors to equate strong recent results with future prospects. But valuation-based approaches focus on expected future returns rather than trailing returns — recognizing that:

- Stocks or sectors that have outperformed may trade at higher valuations and offer lower expected future returns;

- Investments that have lagged may be cheaper and offer relatively better expected returns.

For retirees, valuation focus ≠ market timing; it means aligning your portfolio with a disciplined, cost-effective, diversified strategy that doesn’t shift based on the latest hot sectors.

Reversion to the Mean — A Long-Term Reality

Over the long run, markets tend to drift back toward average performance levels. The original Vanguard projected return chart (unchanged here) shows this principle: asset classes with higher valuations often have lower expected future returns, while those with lower valuations may have higher expected returns.

Short-term leadership does not reliably predict long-term outcomes. A diversified portfolio owns multiple asset classes so that you benefit from broad market growth without betting on a single segment.

Why Diversification Matters for Retirees

For retirees and those preparing for retirement:

- Diversification reduces portfolio volatility, which matters when you’re making regular withdrawals.

- Diversification helps manage sequence-of-returns risk, the risk that early poor returns deplete your portfolio faster.

- A diversified approach is more likely to deliver smooth, reliable outcomes that align with spending needs, not headlines.

If you want a primer on how diversified income flows and drawdown strategies interact in retirement, see our Retirement Income Planning Hub.

For a deeper look at the role diversification plays alongside tax planning and income sequencing, see our Retirement Tax Planning articles.

Related Retiree-Focused Content

- Required Minimum Distributions & Timing — How distribution timing interacts with portfolio longevity

- Social Security Timing Decisions — Income timing considerations unaffected by short-term market performance

- How to Reduce IRMAA — Income planning to manage Medicare premiums

If you’re nearing retirement or already retired, chasing last year’s top performer can undermine your long-term financial security. Staying diversified and disciplined helps align your investment approach with your income needs and risk tolerance. If you’d like a planning-first discussion about how diversification fits with your broader retirement strategy, you’re welcome to Request an Introductory Conversation.